Investing in India in 2026: The Convergent Case, in Fifteen Facts

What does the data actually say about investing in India right now? This note distils our second annual 15 Facts report, fifteen figures, each from a named institutional source and updated to May 2026, into a single convergent argument: the case for a standalone allocation to India.

Why Invest in India in 2026: One Argument, Told in Fifteen Data Points

Historically, most Swiss family offices have had little or no dedicated India allocation; where it exists, in our experience it is usually buried inside a wider regional mandate rather than treated as a region in its own right. UBS’s Global Family Office Report 2025 shows portfolios remain heavily concentrated in Western markets, North America (53%) and Western Europe (26%) together account for nearly four-fifths of assets, while Asia-Pacific and Greater China each draw only about 7%.[1] India is underweight in the indices too, sitting at just 1.9% of the MSCI ACWI IMI, materially below its share of global population and output.[2]

Unfortunately, this under-allocation persists even as the growth gap widens. 2026 has begun under strain, conflict in the Gulf, rising oil prices, LNG shortages, disrupted trade routes, and geopolitical risk is the concern family offices name most often.[1] Yet in its April 2026 outlook the IMF still forecast India growing 6.5% in both 2026 and 2027, against global growth of just 3.1%, the highest rate among the major emerging economies.[3]

The foundation for that growth is structural, increasing resilience to external shocks from within. India's expanding, youthful middle class, combined with a decade of sustained infrastructure investment is laying the groundwork for accelerating, sustained growth in the years ahead. In contrast to previous transformations, like China's, this one can be viewed in real time. India's growth is being built on a digital backbone, further enabling enterprise organisation, while increasing predictability and institutional readiness of Indian investment opportunities. We believe that every emerging market has one decade and this one belongs to India.

The Macro Headline: The Fastest-Growing Top-Ten Economy

India's nominal GDP reached roughly $3.9 trillion in 2025, up 87% over the decade, making it the world's sixth-largest economy, sitting just behind the United Kingdom ($4.0tn), Japan ($4.4tn) and Germany ($5.1tn).[3] The IMF projects India to overtake all three and rank third globally early in the next decade, growing 6.5% in both 2026 and 2027, the highest rate among major emerging economies, against global growth of just 3.1%.[3]

Underpinning that is a demographic foundation that is multi-decade, not cyclical. India is now the world's most populous country at roughly 1.48 billion people, with a median age of 28.1 years, against 39.1 in China, 49.0 in Japan and 45.1 in Germany.[4] Rising incomes, expanding consumption and productivity gains are direct functions of that profile.

From Infrastructure to Real Economic Activity

India’s structural advantages are already translating into output. Under the China+1 manufacturing shift, India has become the world's largest iPhone producer, now assembling 25% of all iPhones globally [5], with smartphone exports surging to $24.1 billion in FY2024–25.[6] It is the combination that is rare: structural cost advantages in production alongside structural scale in consumption.

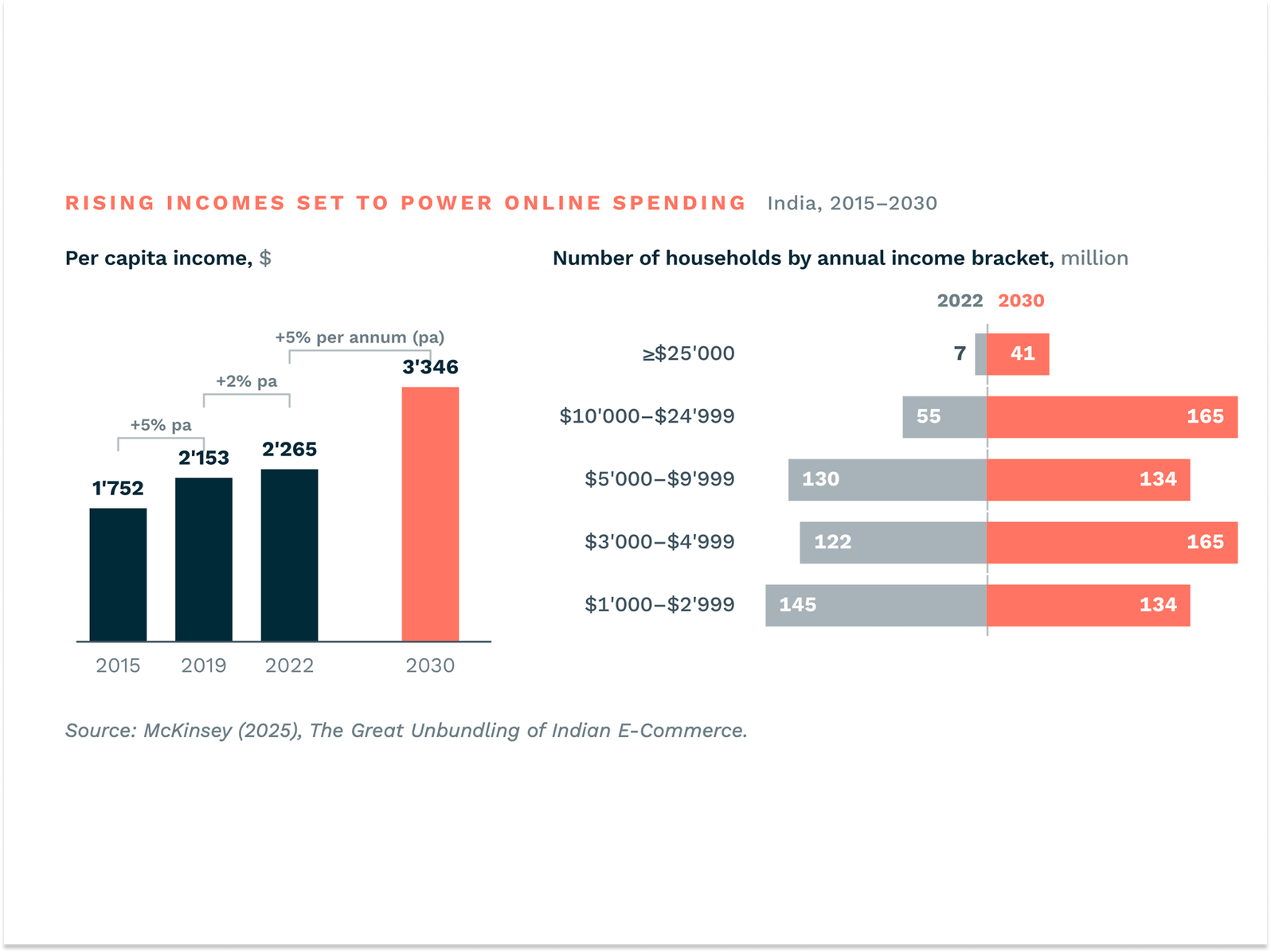

Consumption itself is broadening. India's retail e-commerce market is projected to roughly double to $180–200 billion by 2030, yet only 20–25% of internet users currently shop online, against 85%+ in mature markets.[7] Over 140 million additional households are expected to cross the $10,000 income threshold by 2030, the level at which discretionary digital spending accelerates. And the next wave is coming from beyond the metros: Tier-2 and Tier-3 cities already account for over 60% of e-commerce shipments, with direct-to-consumer sales projected to grow from $10–12bn to $55–60bn by 2030.[7]

Charts showing India's per capita income rising to a projected $3,346 by 2030 and households earning $10,000+ a year expanding sharply, underpinning the consumption case for investing in India

A Decade of Building the Foundation

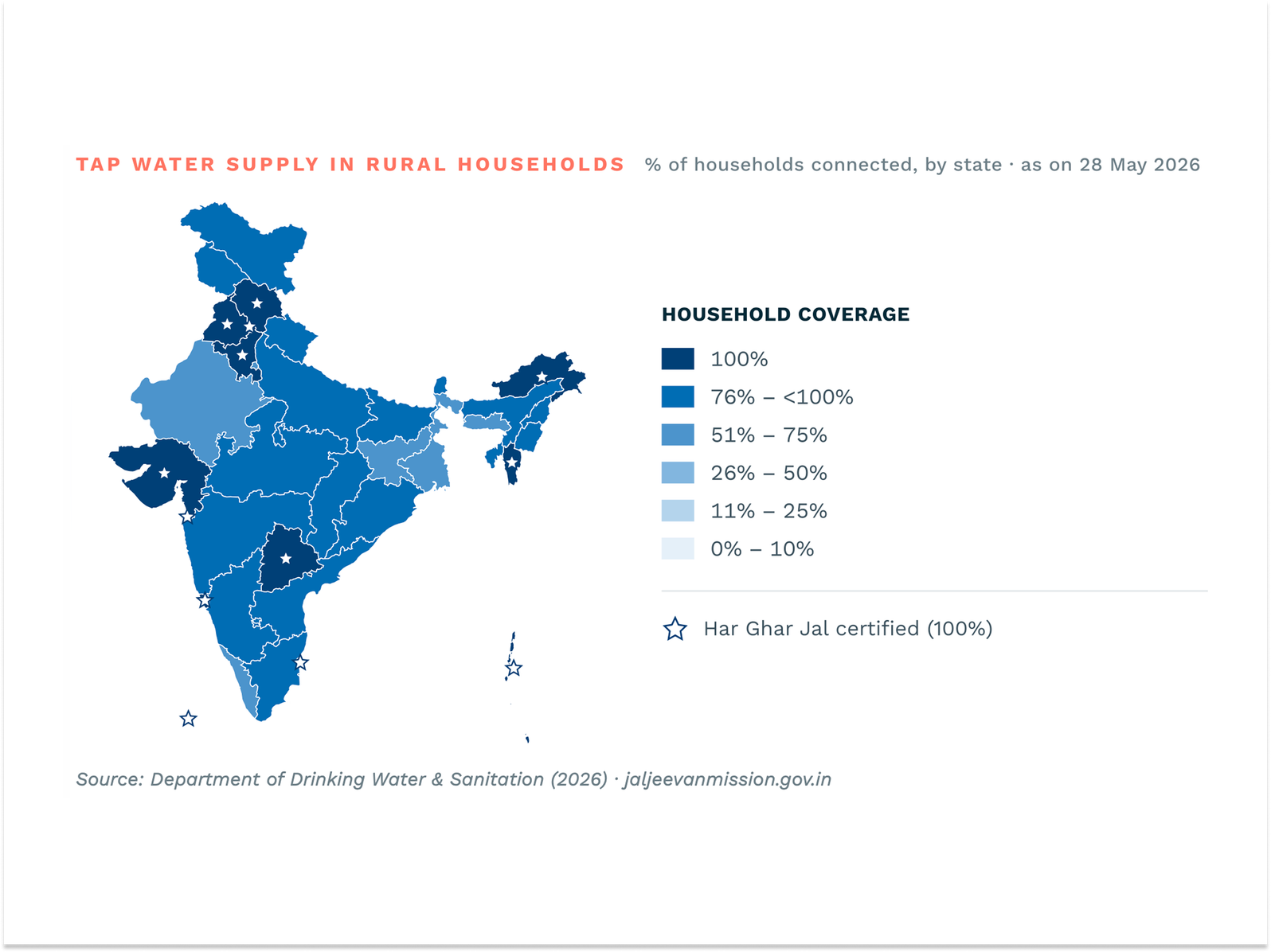

Physical infrastructure has expanded in parallel. India's national highway network grew 61% over the decade, making it the second largest after the United States [8]. Operational airports nearly doubled to 163, with 100 more targeted over the next 10 years.[9] The Jal Jeevan Mission has connected 158 million rural homes to piped water in six years, from under 17% coverage in 2019 to 81.9% today.[10] Clean-water access reduces the disease burden on working-age adults and underpins the household productivity gains that feed rising consumption.

India now ranks third globally in renewable energy capacity at 274.68 GW, overtaking Brazil and crossing 50% non-fossil installed capacity.[11] That build-out matters: as we examined in our note on the supply chain recalibration, India imports the bulk of its LPG through the Strait of Hormuz, and renewable scale is a direct hedge against that import exposure.

Map of India showing rural household tap water coverage by state as of May 2026, with most states at 76–100% connected under the Jal Jeevan Mission

The Access Gap: Where the Opportunity Actually Sits

This is where the fifteen facts converge into a single conclusion.

What distinguishes India's current phase is the simultaneous maturation of three forces –urbanisation, digitalisation and organisation – at a scale no comparable emerging market has combined.

Urbanisation is still early, which is the point. Just 35.4% of Indians lived in cities in 2024, against roughly 66% in China and 80% in the United States.[12] India has added more urban residents since 1960 than the entire population of the European Union, yet it still has decades of higher-productivity migration ahead, each percentage point representing tens of millions moving into higher-consumption environments.[13]

Digitalisation has reached a scale no emerging market has matched. A biometric identity system (Aadhaar) now covers 1.4 billion people, and India processed 129.3 billion real-time payment transactions in 2023, nearly 49% of the global total, more than three times second-placed Brazil.[14] This infrastructure is now the distribution layer for credit, insurance and investment products.

Organisation has advanced on that foundation. Adult financial-account ownership rose from 35% in 2011 to 89% in 2025, one of the fastest expansions of financial access on record.[15] For scale: State Bank of India alone serves around 520 million customers [16], roughly 58 times the population of Switzerland. India's internet base has now crossed one billion users, the world's second-largest, on penetration of only ~70%, meaning the runway is still long.[17]

A Maturing Capital Ecosystem

The data establishes where India’s growth is occurring: across an unlisted majority, in Tier-2 and Tier-3 cities, in sectors benefitting from structural tailwinds. The harder question is how to access it.

India’s structural momentum is already drawing institutional capital at scale. 2025 was the second-highest year of private capital deployment on record, at $60.7 billion across 1,475 deals, with PE/VC exits of $32.9 billion and India-focused fundraising hitting an all-time high of $23.2 billion, more than double the prior year.[18] India has also led the world in IPO listings for two consecutive years, with 367 in 2025 and another 54 in Q1 2026.[19] The opportunity itself is not going unnoticed, yet traditional private equity funds typically require 10 year lock up.

The public route comes with a catch: the MSCI India Index trades at a 33% premium to the emerging-markets average (a 24.6× trailing P/E) [20], and that premium is concentrated, the top 10 stocks make up nearly 30% of the Nifty 500, Financial Services alone over 30%.[21] Fewer than 1% of India’s registered enterprises are listed on any exchange.[22] A listed-only allocation buys a narrow, expensive slice.

That is the access gap. As the under-allocation amongst European investors interested in India shows, they have so far responded in one of two ways: foregoing a dedicated India allocation altogether, or accessing the market through instruments only partially suited to its structure.

Read the Full Report: 15 Facts on India

For European allocators, the choice of vehicle matters as much as the decision to allocate. To explore specific India investment opportunities, or discuss how a dedicated India allocation could fit your mandate, get in touch with the RootBridge team. Klick here to download the full report.

- UBS (2025). Global Family Office Report 2025.

- MSCI (2025). A Complete Geographic Breakdown of the MSCI ACWI IMI

- International Monetary Fund (2026). World Economic Outlook, April 2026. imf.org

- UN DESA, Population Division (2024). World Population Prospects 2024.

- Bloomberg (2026). Apple now makes about 25% of iPhones in India after China pivot.

- Statista (2025). India's Smartphone Exports Surge.

- McKinsey (2026). The great unbundling of Indian e-commerce.

- Ministry of Road Transport & Highways (2025) Year End Review 2025.

- Ministry of Civil Aviation (2026) Government of India.

- Jal Jeevan Mission, DDWS (2026). JJM Dashboard.

- Ministry of New & Renewable Energy (2026). Government of India.

- UN Population Division (2024). World Urbanization Prospects: 2024 Revision.

- Ritchie, H., & Roser, M. (2024). Urbanization. Our World in Data.

- ACI Worldwide (2024). Prime time for real-time global payments.

- World Bank (2025). Global Findex Database 2025.

- State Bank of India (2025). Annual Report 2024–25.

- World Bank (2026). Individuals using the Internet (% of population)

- EY (2026) How India’s PE/VC ecosystem is sustaining momentum amid global volatility

- EY (2026) Global IPO market stabilises in 2025 while 2026 pipeline signals potential AI-led mega wave

- Siblisre Rearch (2026) Emerging Markets Equity Valuations

- NSE (2026), Nifty 500

- Udyam Registration Portal (2026). Government of India.

Get your newsletter.

Never miss a chance to unlock insights and opportunities in the world’s fastest-growing economy. Sign up for our newsletter today.

Thank you for signing up

You're officially on the list. Fresh updates, insider news, and exclusive content are headed your way. We're glad to have you with us!